If you intend to live and work in Amsterdam or anywhere else in the Netherlands then it is absolutely essential that you have a local Dutch bank account. Generally, standard bank accounts can be opened once you have an income in place.

To open a bank account you normally need to visit a branch in person, preferably near to where you live or work with various documents in-hand. However, some banks are now allowing applications to be done online.

When you register with the authorities in the Netherlands you will receive a Burger Service Nummer (citizen service number). This is used as both a fiscal number for dealing with tax and also as a general identifier for government services and healthcare. You will normally need to provide a bank this number when opening an account or later on.

Documents required to open a branch bank account

To open a standard Dutch current account from one of the main retail banks you will need to bring the following documents with you to the bank in order to satisfy the usual know-your-customer procedures:

- Identity Document – This should be a valid passport (Dutch or international); a valid Dutch driving license; an identity card from certain EU countries may also be accepted. If you have a residence permit card you should also bring this.

- BSN number – Burger Service Nummer (citizen service number).

- Proof of Address – The bank may sometimes ask for proof of address such as a rental contract for your house/apartment or a recent utility bill.

- Proof of Income – The bank will require some evidence of income in the form of an employment contract, recent pay slips or a statement of employment benefits. Without any income you might not be allowed to open a standard current account. Students should bring proof of enrollment at their university or educational institution.

Also see How much money will I earn in the Netherlands?

However, with the introduction of mobile banks and retail banking apps, it has become a little easier to set up banking facilities in the Netherlands.

Banks in the Netherlands

The big 3 retail banks in the Netherlands (ABN AMRO, ING and Rabobank) have significant market share.

Mobile banks are becoming ever popular particularly with the younger generation and offer a raft of mobile app-based features. Accounts are generally easier to open than those of standard retail banks.

ABN AMRO (abnamro.nl)

[RECOMMENDED for EXPATS] The popular Dutch banking giant has branches all over the country. ABN AMRO has a special international clients division so it is well used to dealing with expats, particularly in the main city branches. It offers internationals a full range of financial services such as bank accounts, insurance, investments and mortgages.

In addition it also offers current accounts and insurance packages for international students in the Netherlands; it also has a specialist desk for dealing with international high flyers in the sport and entertainment fields.

ABN AMRO has an extensive English version of its website, internet banking portal and mobile banking app. It can provide correspondence and documentation in English where possible, although legal agreements will usually be in Dutch.

It is possible to open an ABN AMRO account online here (English) in around 10 minutes without the need to visit a branch by using the ABN AMRO app.

Applications through the app are possible if you are aged 18 or over and are tax resident in the Netherlands with an official Dutch home address. You need to upload a copy of a valid Dutch identification document, residence permit or international passport (US passports are not accepted). You also upload a photo of yourself and answer some questions.

An ABN AMRO bank account with a debit card costs €3.25 per month (€39 per year).

As a side note, the name ABN AMRO originates from 2 Dutch banks which merged in 1991 – ABN bank (Algemene Bank Nederland) and AMRO bank (Amsterdam and Rotterdam Bank). ABN AMRO was purchased by a consortium of Royal Bank of Scotland / Santander / Fortis in 2007.

Following the financial crisis, the bank was nationalised in 2009 by the Dutch government along with Fortis Nederland. In 2015 it was partly relisted on the Dutch stock exchange and the government is slowly reducing its shareholding.

bunq (bunq.com)

[RECOMMENDED for EXPATS] A mobile app-based Dutch bank officially launched in 2015 with international portal available in English, Dutch, French, German, Italian, Portuguese and Spanish – making it a smart choice for expats.

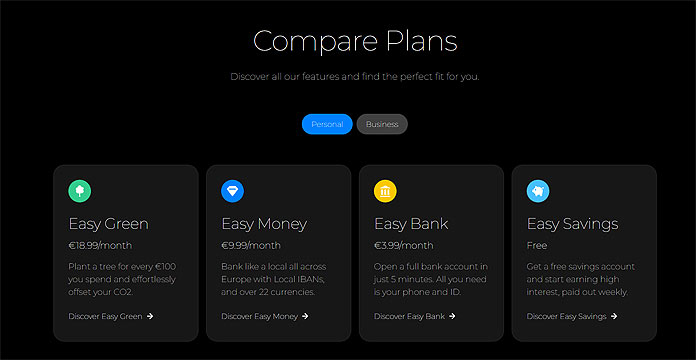

For personal customers it has the following plans:

Easy Money – Its most popular plan at €9.99 per month which offers multiple European IBANs, up to 25 sub-accounts in 16 different currencies and the possibility to make investments.

Easy Green – A ‘sustainable’ banking product at €18.99 per month. It additionally offers a metal card with purchase protection and ‘a tree is planted for every €100 spent’.

There is also a base Easy Bank plan (€3.99 per month) with more limited features and a free Easy Savings product.

- the virtual bunq Mastercard has no forex fees for non-Euro foreign currency payments and can be used with Apple Pay or Google Pay.

- The bunq app has instant notifications on transactions and makes it easy to set budgets and open sub-accounts.

- The bunq credit card has a 2% cashback available for public transport expenses (Easy Green users) and a 1% cashback (Easy Green/Easy Money users) for restaurant/bar expenses.

- bunq gives a free 30 day trial of all plans.

- bunq plans are also available as business accounts.

- Easy Savings is one of the market leaders for savings interest rate at 2.46% for up to €100,000.

Opening a bunq account can be done in just 5 minutes – as long as you have your ID at hand and a European address. You can even open an account if you don’t yet have your BSN number. Open a bunq account here (English).

bunq is fully registered as a bank in the Netherlands and is covered to €100,000 by the Deposit Guarantee Scheme (DGS).

ING (ing.nl)

Internationale Nederlanden Groep is a major international banking, insurance and asset management group. It became the largest Dutch retail bank after taking over the old Post Office bank Postbank which was re-branded as ING.

Non-Dutch nationals can open an ING account if they have a link to the Netherlands. You would need to show the following documents in the branch:

Your main identity document plus one of the following:

- if you live in the Netherlands you can show an extract from the Dutch Personal Records Database (BRP) from your local authority.

- if you work in the Netherlands you can show an employment statement.

- if you study in the Netherlands you can show proof of enrollment with the educational institution.

- If you own a house in the Netherlands, you will need to present an ‘Eigendomsinformatie‘ (Ownership Information) document.

ING offers an English version of its mobile banking app and online banking portal. It is also now possible to apply online through the app if you have a Dutch address, valid European ID (and residence permit). You need to upload a copy of your ID and take a selfie.

ING current account packages start at €3.20 per month.

N26 (n26.com)

An app-based bank based in Germany which offers mobile banking throughout Europe.

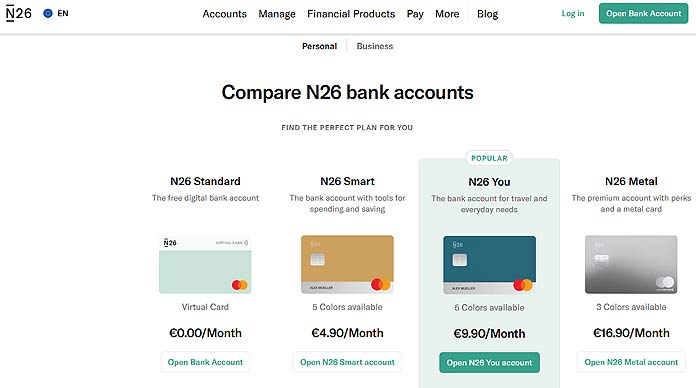

The standard N26 account is free, the N26 Smart account costs €4.90 per month, a premium N26 You account costs €9.90 per month and the N26 Metal account costs €16.90 per month. Account holders are issued with a Mastercard debit card.

Standard account holders get a virtual card or a physical Mastercard debit card (€10 delivery fee) with 3 free monthly withdrawals in euros per month, non-euro transactions having no forex fee.

The N26 You account offers fee-free withdrawals worldwide and Allianz travel insurance coverage.

The N26 Metal comes with a metal card and has additional mobile phone and car rental insurance coverage.

Any transactions on N26 cards comes through as instant push notifications on the app. Google pay and Apple pay is included. Support is available in English, French, German, Italian and Spanish. Accounts can be opened in 8 minutes via the app – you will need to download the app and produce ID.

Balances up to €100,000 in N26 are guaranteed by the German deposit scheme.

Knab (knab.nl)

An online and app-based bank set up in 2012 by financial group Aegon. As of 2024, it is owned by BAWAG Group AG, an Austrian firm.

Knab has almost 400,000 customers, 270,000 of which are entrepreneurs. It offers the following packages:

- a standard Knab Plus account (Privérekening) is €6 per month. The joint account (Gezamenlijk) is €7 per month.

- This includes up to 5 sub-accounts and the possibility of applying for a free credit card.

- a business account (Zakelijke rekening) is €7 per month which offers 5 sub-accounts and 500 free transactions per year.

Knab offers package holders various savings products and other financial services such as investments, crowdfunding and mortgages.

Knab does offer a customer service contact option via telephone (0800-2000 daily).

The Knab online portal is only available in Dutch.

Rabobank (rabobank.nl)

This is a privately owned Dutch bank and financial services group with roots in agricultural and cooperative finance. In terms of the big 3 Dutch retail banks, it is the second largest bank by assets and has slightly higher credit ratings from the international agencies.

Rabo has many branches in Amsterdam and all over the Netherlands. Rabobank has only recently introduced some English overview pages on its website – but application pages are in Dutch.

To set up an account with Rabobank you should visit one of their main city branches. it is possible to open an account via the Rabo App but this is in Dutch-only.

Accounts start at €2.95 per month.

SNS Bank (snsbank.nl)

SNS stands for Samenwerkende Nederlandse Spaarbanken (Co-operative Dutch Savings banks).

Since 2017, this Dutch retail bank has been part of De Volksbank group which is owned by the Dutch state following a nationalisation of SNS in 2013.

SNS Bank has about 200 branches in the Netherlands, with 2 in and around central Amsterdam – at Kinkerstraat 158 and Ceintuurbaan 292 HS. It has automatic teller machines (ATMs) located in HEMA stores.

SNS provides banking and financial services to retail customers with all its online and banking services being in Dutch.

ASN Bank (asnbank.nl)

A small Dutch online bank (also part of De Volksbank group) headquartered in The Hague and focussed on ethical banking and sustainable investments.

The bank is branchless so accounts can only be applied for online – you also need to post a copy of your identity document. No English language info or products are available. ASN requires that you already have a Dutch bank account, so this not really an option for arriving expats.

Triodos Bank (triodos.nl)

Also a small ‘ethical’ Dutch bank which offers an online current account and other financial products. As with ASN, accounts can be applied for online and documents need to be posted – it takes around one week to set up an account. Triodos has no branches but does have an office in Zeist (near Utrecht).

There are no English products available for Dutch-based clients though Triodos does have an English website for the UK market.

Van Lanschot Kempen (vanlanschotkempen.com)

The oldest independent bank in the Netherlands which dates back to 1737. It offers private banking current accounts and other financial services and has a particular focus on entrepreneurs, professionals and high net-worth individuals. It has no English info on its main website.

Headquartered in ‘s-Hertogenbosch, it has a single branch office in many Dutch cities including Amsterdam at Apollolaan 150.

For non-Dutch speaking internationals setting up in the Netherlands, probably the best banking bet is going with either Dutch retail bank ABN AMRO (apply here) or local mobile bank bunq (apply here). This is followed by ING and mobile bank N26. For those who can speak Dutch or have Dutch friends/colleagues or partners to assist, then you have more choice of banks.

How Dutch bank accounts work

Once your current account (betaalrekening) is confirmed you will get an international bank account number (IBAN) code which has 18 characters in the Netherlands. Each bank also has a special BIC identifier code, for example ABNANL2A for ABN Amro.

You will shortly receive a local debit card (betaalpas or more commonly known as PIN pas) which can be used to withdraw cash at ATMs (geldautomaat) and make chip and pin or contactless payments at retailers. The card is either Maestro (Mastercard) or V-Pay (Visa) branded as the old Dutch PIN branding has been phased out.

Contactless payments have a limit of €50 per transaction with a PIN needed after each €100 of consecutive payments.

The debit card also allows international transactions – Euro currency withdrawals in the eurozone are generally free but you will be charged for foreign currency (non-euro) transactions.

Expect a monthly charge for running a current account and debit card – this will range from about €3 to €7 per month, depending on additional services included in your banking package.

Credit cards in the Netherlands are slowly becoming more accepted though a number of Dutch retailers still won’t accept them.

Dutch internet banking and mobile banking are popular and can be easily set up with your account. Some banks will send you a special card reader or number generator for use when logging in and/or making online transactions.

An online payment system called iDEAL is used by many Dutch online retailers which links securely to your internet banking portal to make direct payments without charge. Look out for the following logo:

Note that due to issues with international fraud, Dutch banks default the debit cards for use only within Europe. You must (temporarily) set it to “worldwide use” using internet/mobile banking if you want to make withdrawals outside Europe. You can also change the maximum daily withdrawal amount which is generally set at either €250 or €500 per day.

Bills in the Netherlands are generally paid either by direct debit or online bank transfer. Many transfers are made using the acceptgiro system where the payment has a special reference number which is quoted during the transfer.

Note, standard cheques are not used in the Netherlands – if you deposit a cheque into your account (even if denominated in euros) you will likely be charged a hefty €15-€20 for the privilege.

Once your main current account is set up, you can easily open a savings accounts (sparen). You will find slightly higher interest savings rates on offer from either smaller banks or foreign banks.

For a listing see Savings Accounts Rates in the Netherlands

Investment accounts (beleggen) can also be set up at most banks or by using a specialist broker such as Binck. Ethical investment products are available with ASN and Triodos Bank – some of which are exempt from Dutch wealth tax.

Note, Dutch bank deposits are officially “guaranteed” up to €100,000 by the Dutch central bank. A temporary 3 month guarantee up to €500,000 is given for proceeds of a house sale. If you have more than €100,000 in savings then at least spread it around different banks or consider other international diversification strategies.

Last updated 9 April 2024. This article was first published in 2010 and has been regularly updated.

Links on AmsterdamTips.com may pay us an affiliate commission.